Customer Acquisition Cost (CAC)

-

1Video

-

-

2How To Calculate CACA very important customer-focused metric business owners need to understand is Customer Acquisition Cost (CAC), which goes hand-in-hand with Customer Lifetime Value addressed in a separate article that can be viewed here. CAC is simply the amount of money a company has to spend to gain a new customer. It is a key indicator of whether marketing and sales activities are successful.

CAC is a business's total cost of sales PLUS total cost of marketing divided by the total new customers in that same period. New customers are unique customers that have never purchased from the business previously.

What makes up COS & Marketing?

Examples of what can make up the top part of the CAC equation could include:- Sales & marketing sales salaries

- Cost for items that go into the sales process

- Advertising expense (paid, organic search, etc)

- Marketing expense

- Content creation/social media costs

- Other direct costs in the acquisition cycle

Customer Types

- New customer - unique customer purchasing for the first time

- Recurring customer - existing customer who repeatedly purchases typically via a subscription type model

- Reoccurring customer - existing customer who purchases but not on any sort of regular basis

EXAMPLE:

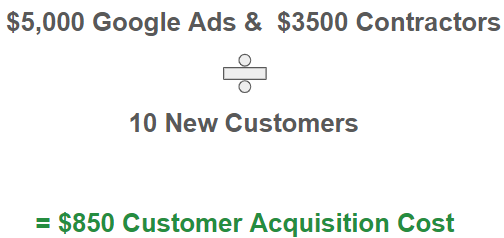

A business had $5,000 of Google ad spend throughout the year and paid one Marketing Contractor $3,500 during that same year.

As a result, 10 new customers were acquired. Based on the money that was spent, the Customer Acquisition Cost for the business is $850.

-

3Effectively Using CAC with CLVIn the example above, the Customer Acquisition Cost for the business is $850. The company now needs to ask itself, "Is that a good or a bad thing?" The answer is "It depends."

The CAC in itself is just data and now the company needs to take that data and put it to use by comparing it to the Customer Lifetime Value (CLV) metric previously mentioned. Knowing the CAC and CLV, the business can determine how much they can spend to acquire a new customer.

The general CLV metric that a company should strive for is 3:1 to the acquisition cost. This ratio means that a business can spend right up to that amount to acquire that customer. If the ratio is less than three to one, the business could be spending too much to acquire their customers.EXAMPLE:

Starbuck has a reported CLV of $25,000. Knowing this, Starbucks can use this information to aggressively target and acquire new customers. Using the 3:1 CLV to CAC ration, they know they can spend up to $8,000 to acquire one new customer.Reducing CAC

That's just a metric that a lot of people try to, to strive for. So the next key point, right, is understanding how to reduce your customer acquisition cost.- Figure out where customers come from

- Control costs and improve close rate

- Measure CAC on a consistent basis (i.e., monthly, quarterly)

The business should focus on the different advertising or marketing channels being used and determine what is working and what is not. Being able to track where customers come from will enable the business to decide where or how to best shift, or even eliminate, marketing dollars. Monitoring on a regular basis will allow the business to increase their CLV.

Did this answer your question?

If you still have a question, we’re here to help. Contact us