Augusta Rule - Deep Dive

One of our favorite tax strategies for business owners is called the Augusta Rule. Simply put, the Augusta Rule is a tax loophole that allows homeowners to rent out their home for up to 14 days per year without a rental income reporting requirement on their personal tax return. Officially known as Internal Revenue Code Section 280A(g), the nickname originated with Augusta, Georgia homeowners using the tax code to their advantage when renting out their homes to annual Masters golf tournament attendees and enjoying the benefit of tax-free income! The Augusta Rule can be used by any taxpayer who owns a home in the United States, provided that the home is NOT the primary place of business. Here we will discuss how you can maximize it as business owner and what to stay away from as well.

-

1Video

-

-

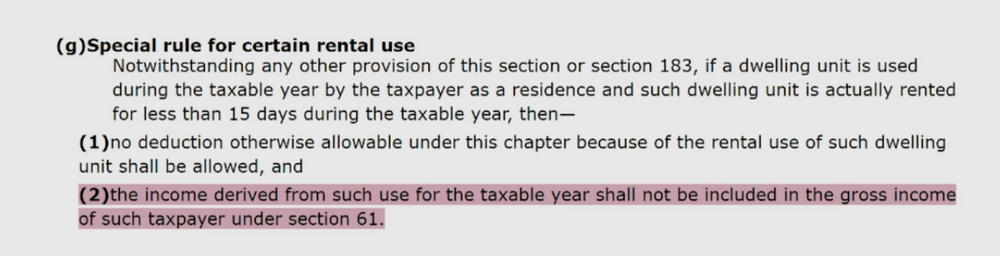

2The Augusta Rule aka Internal Revenue Code Section 280A(g)The Augusta Rule is a unique provision in the Internal Revenue Code under Section 280A(g) that many business owners should take advantage of.

At its most basic premise, the provision states that a taxpayer may rent out their personal residence for up to 14 days and NOT have to report the income as taxable income on the taxpayer's personal tax return. Specifically, this code refers to gross income:

Following the rules and regulations under this section of the tax code, a taxpayer can:- Maximize the rental expense write-off to their business, AND

- Put rental income in their pocket as an individual and not be required to pay tax on it.

It is essential that this strategy is implemented properly so the business owner can maximize the benefit on both the business side as well as the personal side and to ensure the IRS will not disallow it. -

3Using the Loophole to Your Advantage

Schedule Off-Site Business Meetings at Your Home

There are many different tips and tricks available but it's important that the business owner focus on what has proven to be acceptable by the IRS and what can be used to produce the highest return on investment.

Key to what the IRS says is that an individual can rent their home to their separate business, the business pays rent to the individual for use of the home, and the individual does not have to report it as gross income on their tax return.- Business Meetings

- Entity must be an S-Corp, C-Corp, or Partnership taxed as an S-Corp or C-Corp.

- Meetings can include those with prospects, colleagues, clients, board members, etc.

- Allows the business owner to hold meetings at the owner's home.

- The business owner is renting out the home to the business.

- The business is considered the renter

- The business owner is considered the vendor

How to Apply It?

- From a transactional perspective, the business meeting is a rent expense to your business.

- Rent is paid from the business to the individual, at Fair Market Value

- If the home is rented 14 days or less during the year, no requirement to report it on the individual tax return.

- Once the home is rented for the 15th day, the tax advantage is lost and the individual must report the income.

- Although it does not have to be reported by the individual, it does get treated as a "debit" or increase to rent on the business's books

- This becomes a deduction to the business and is tax free personal income for the business owner.

Maximizing the Strategy

Business owners inevitably hold meetings in the daily course of doing business, whether on-site or off-site. Many think that those meetings need to be in traditional locations such as on-site in the business owner's office, at a restaurant, or at an off-site conference center. By taking advantage of the Augusta Rule, business owners change the traditional mindset of where a meeting has to be held and maximize the benefit the code offers.- Fair Market Value is Key

- First and foremost, the IRS requires the fee established to rent the home be at a justified fair market value (FMV) for the area.

- Do the research and come up with three different market comparisons to show that the rate being charged is FMV. Comps could include hotel venues, Airbnb, or Peerspace.

- Document the comps and set a reasonable FMV rate based on those comps so in the unlikely event of an audit you are able to prove to the IRS that the rent established is FMV.

- Business Deduction

- There are three ways to get money out of your business: 1) wages, 2) distributions, or 3) expense reimbursement.

- The August Rule strategy falls under the third category, expense reimbursement since the business owner is taking money out of the business with no tax consequences.

- The business has agreed to reimburse its shareholder employee who owns the residence being rented.

Example: A business owner wants to rent out their residence to the company, which has $100,000 net operating income. - The business owner researches the comparable rents for the area.

- The owner comes up with a $1,000 fair market value for a one-day rental of their personal property.

- Renting out the residence to the business 14 times per year equates to a $14,000 deduction to the business.

- From a transaction perspective, the deduction brings the business's operating income down to $86,000, reducing the amount the business is taxed on by $14,000.

- The rent paid out is not really being spent but is transferred over to the business owner personally as rental income, tax free as long as this is done 14 times (days) or less.

- So you took it in tax free, But you're actually paying taxes on $86,000 now. It's really a double whammy. So that is really the trick to it

How to Utilize the Strategy When There are Few to No Employees

One of the best ways to exercise the Augusta Rule for a small business with few or no employees is by appointing an internal Board of Advisors. A Board of Advisors (BOA) is similar to a Board of Directors, but a BOA exists in a limited capacity for LLCs.- The business can appoint anyone to the BOA, including family and friends who give business advice.

- The BOA formation is not a public declaration, rather is done with an internal document showing that the business is appointing certain individuals the the BOA.

- Highly recommended that the BOA election is done formally so that it is documented.

- With the BOA established, the business owner can now have formal business meetings at the business owner's residence and use the Augusta Rule to take advantage of the deduction for the business and tax-free income personally.

- Beyond the August Rule, establishing a BOA means the business is able to increase meal and travel expenses when meeting with the BOA.

Meeting Minutes are a Must

Documentation is one of the key components to ensuring the August Rule works to your advantage.- Whenever a business meeting is held at the business owner's residence, someone should be tasked with recording the meeting minutes to document the details of the meeting:

- Date and time of the event

- Who attended the meeting

- What was discussed

- What was the outcome

- Where it was held and at what rental rate

- In the event of an audit down the road, documenting the meeting minutes will allow you to prove the deduction was a legitimate business expense.

- Business Meetings

-

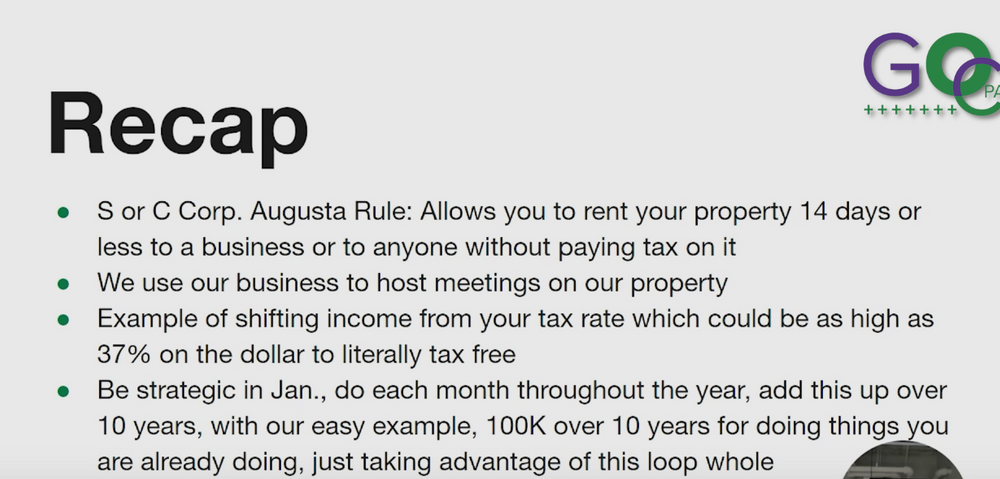

4Augusta Rule Recap

- Applies to entities that are taxed as S-Corp and C Corp.

- The concept relates to income shifting from the business to the business owner.

- Allows the business to hold meetings up to 14 days and deduct the rental expense, thereby lowering the total income that is being taxed at the current tax rate.

- Gives the business owner up to 14 days of tax free rental income as an individual from the business that is not required to be reported on the personal income tax return.

- Start early. Begin in January and hold meetings once per month and include a few holiday meetings to reach that 14 times maximum.

- Over ten years, this results in a powerful ROI.

- Think about $10k over 10 years. That is $100,000 of tax deductions otherwise left on the table!

- Reinvest tax savings somewhere else to increase the ROI even more.

-

5Anomaly Can Help You Implement the Augusta RuleThe August Rule is a unique planning opportunity that can be extremely lucrative.

The Anomaly team has worked with many companies to help them incorporate this strategy into their business.

If you are interested in learning more about how this can work for you, please reach out to our team in Soraban.

Did this answer your question?

If you still have a question, we’re here to help. Contact us