I Got An IRS Letter...What Now?

Not surprisingly, letters or notices from the IRS often cause taxpayers anxiety simply because the IRS has contacted them. The first thing we advise taxpayers is not to panic. IRS letters are quite common and the vast majority of these letters are actually computer-generated resulting from data mining conducted by the IRS AUR (Automated Underreporter) program. This program matches information provided by the taxpayer with information provided by third parties that are reporting to the IRS. If there is a mismatch of information, a letter will automatically be generated.

In addition to a discrepancy in information being reported, the IRS will also send out letters for verification purposes. The IRS may want to verify a taxpayer's identity, address, income, and withholdings, among other things. Also, receipt of an IRS letter does not automatically mean you are being audited. An audit letter is very different from a normal IRS letter and it is very clear that the taxpayer has been contacted because of an audit. The vast majority of letters are just informational or adjustment-based notices so that the taxpayer understands what information the IRS has on the taxpayer's IRS account.

In this article we will discuss the most common type of letter that the IRS sends out and what steps should be taken to address it.

In addition to a discrepancy in information being reported, the IRS will also send out letters for verification purposes. The IRS may want to verify a taxpayer's identity, address, income, and withholdings, among other things. Also, receipt of an IRS letter does not automatically mean you are being audited. An audit letter is very different from a normal IRS letter and it is very clear that the taxpayer has been contacted because of an audit. The vast majority of letters are just informational or adjustment-based notices so that the taxpayer understands what information the IRS has on the taxpayer's IRS account.

In this article we will discuss the most common type of letter that the IRS sends out and what steps should be taken to address it.

-

2Examples of Common IRS LettersOne of the most important things to know about IRS notices or letters is that they will always be sent via mail. The IRS will not initiate a notice with a phone call, email, or text so any initial communication via one of these methods is not legitimate.

A few examples of common IRS notices are:CP 2000

- The IRS is proposing an adjustment to a tax return that was filed.

- The notice alerts the taxpayer that the income or payment information provided on the tax return does not match what the IRS has on file.

- The notice will provide the information used to calculate the adjustment.

- The adjustment may result in an increase or decrease in tax liability, or it may even result in no change at all.

- Taxpayers have the opportunity to respond to the notice using the response form included with the notice.

CP501

- A CP501 notice is issued when there is balance due to the IRS.

- This could result from adjustments that have already been made (i.e., resulting from a CP2000 notice) and for which payment of the tax is now due.

- Pay attention to the due date to avoid accruing additional penalties and/or interest.

- An appeal can be requested if there is a disagreement with the amount owed.

- The IRS has payment plan options if the full payment cannot be made by the due date.

CP05

- The IRS will send a CP05 notice to let the taxpayer know it is verifying income, income tax withholding, tax credits and/or business income reported on a tax return.

- If a tax return has been filed, the taxpayer does not need to take any action until 60 days after the return has been filed and only if the refund has not been received or the taxpayer has not heard from the IRS again.

- If a taxpayer has not filed a return but does receive a notice related to a tax filing, the taxpayer should review the IRS's Taxpayer Guide to Identity Theft for information on steps that can be taken to ensure identity security.

-

3What To Do Upon Receipt of an IRS Notice

- Read the Notice - The first thing to do is read the letter in its entirety. Depending on the notice type, it will provide important information the taxpayer will need to know, such as:

- An explanation for why the notice was issued

- Information the IRS has on file compared to what was reported

- The due date for a response from the taxpayer

- A response form that details what actions can be taken

- Locate the Notice Reference Information - Make note of the notice information located in the upper right corner:

- Notice number (i.e., CP2000). you can Google the notice number to get information about that type notice

- IRS phone number to call

- Due date for a response or payment

- Pay Attention to the Due Date- If there is a deadline to respond, put it on the calendar.

- If a deadline is missed, it can cause even bigger issues down the line

- Contact a Professional - Contact GO CPA for assistance if there are any questions about any notice received. A tax professional will be looking out for the best interest of the taxpayer, not the IRS, and will be able to help the taxpayer understand the notice and how to respond appropriately.

- Read the Notice - The first thing to do is read the letter in its entirety. Depending on the notice type, it will provide important information the taxpayer will need to know, such as:

-

4CP2000 ExampleThis example will go through a CP2000 proposed adjustment notice to illustrate how, as a tax professional, we would address this type of notice. One thing to keep in mind is that this type of notice is not a bill. It is notifying the taxpayer of changes the IRS believes should be made to a tax return.

It is important to understand the IRS notice. Many taxpayers' first reaction is to pay the amount due shown on the notice so the IRS doesn't come after them. Even if it turns out the taxpayer owes additional money, paying the amount shown on the notice without looking into the issue is a bad idea. The IRS can, and does, make mistakes so it is to the taxpayer's advantage to thoroughly review the notice and understand what caused the proposed changes. This will give the taxpayer the opportunity to dispute changes that are not accurate.Initial Steps

- Forward the notice to a professional - If sending this letter to a CPA or tax professional, an attorney, or even an in-house accountant for your business, make sure ALL pages of the notice are sent. Each page has important detail related to the issue at hand and are necessary to fully understand what the notice means and how to respond.

- Request additional time - If more time is needed to review the notice, contact the IRS at the number provided on the notice as soon as possible. This is very important because once the deadline on the notice for a response has passed, penalties and interest will accrue.

- Review the notice - Compare the tax return and supporting data in question to the proposed changes outlined in the notice to check for inaccuracies in what the IRS has proposed based on information they say has been reported to them.

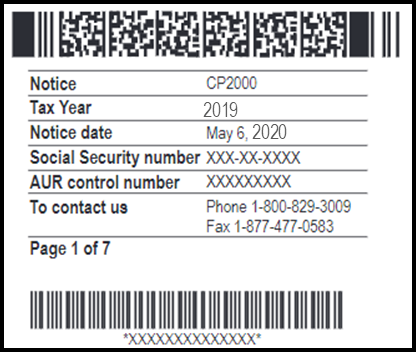

Notice Reference Information

In the upper right corner is important information that will be needed when contacting the IRS:- Notice Number - This identifies the type of notice the IRS has issued

- Tax Year - What is the tax year to which the notice pertains

- Notice Date - The date the noticed was issued

- Social Security Number - The taxpayer's TIN

- AUR control number - The reference number the IRS will use to identify the notice

- To contact us - IRS contact information for inquiring about or responding to the notice

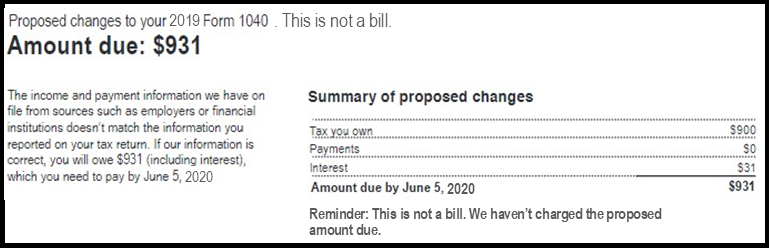

Proposed Changes

This section will give a summary of the proposed changes and go into detail of exactly what the proposed changes to a tax return are and how the proposed changes affect the tax filing (i.e., additional amount due, refund, no change). Remember, the CP2000 notice is not a bill from the IRS. It is simply a notification to the taxpayer of changes the IRS believes should be made to a tax return.

The Summary of Proposed Changes provides a short calculation of what the proposed changes are, including any penalty and interest. The due date for a response is shown here and is the date by which the taxpayer needs to respond, whether agreeing to or disagreeing to the proposed changed, in order to avoid an increase in penalties and/or interest.

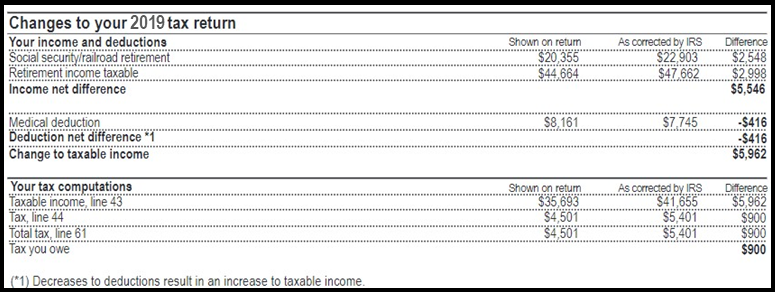

Changes to the Tax Return

This section will show the specific calculations that the IRS used to come up with the proposed changes. NOTE: This section does not include the calculation for penalties and/or interest.

Tax Computations- These calculations will show each item associated with the discrepancy, the adjusted amount, and the difference. The following columns show the information as the IRS has it in their records:- Shown on return - This is the original amount as reported on the filed tax return

- As corrected by IRS - This is the adjustment made by the IRS

- Difference - This is the difference between the first two columns (listed above) and will be the additional amount due, amount to be refunded, or reflect no change to the tax return

Payments - This section will show any payments the IRS has documented to have been made related to the tax period to which the notice pertains. This section will show tax withheld from W2 wages as well as any estimated tax payments made.

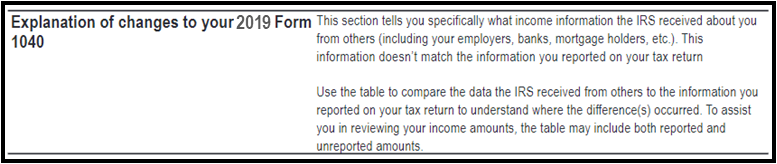

Explanation of Changes- This section will go into detail about the specific information the IRS has from third parties which does not match what was reported on the tax return.- The IRS will go by the third parties' reporting unless the taxpayer can provide documentation that disputes the information the IRS has and supports the taxpayer's stance.

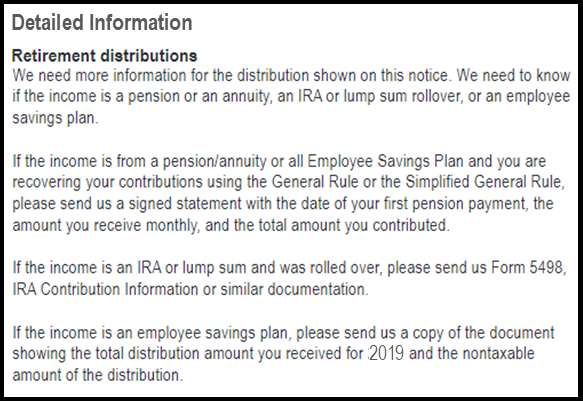

Detailed Information- The IRS will request specific information in order to more accurately calculate the proposed adjustment- This section is not always on the CP2000 notice

- Oftentimes this is where the IRS may be incorrect with their adjustment and a response to argue the adjustment is necessary.

Power of Attorney (POA) - This notation will be on the notice if there is an IRS Power-of-Attorney on file. The IRS will send a copy of the notice to the taxpayer's POA, such as a CPA, attorney, EA, or other tax professional designated as POA.Next Steps - Response Form

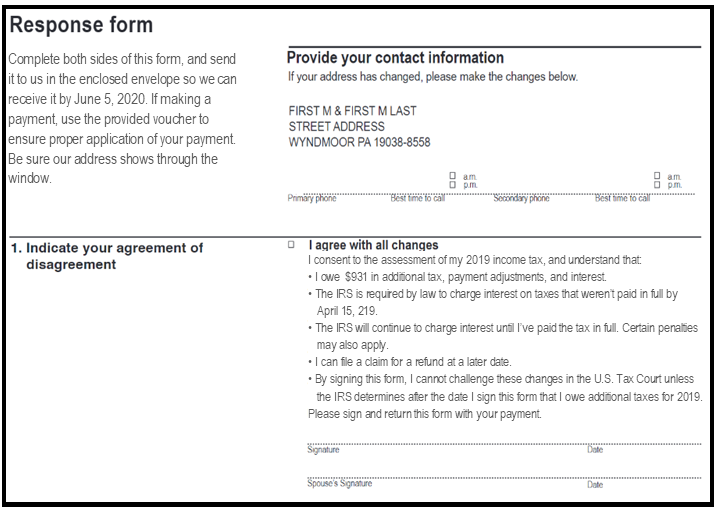

The CP2000 will include a Response Form allowing the taxpayer to respond that they agree with the notice or contest the proposed changes. Remember, if the IRS does not receive a response by the deadline as posted the notice additional penalties and interest will accrue.- Indicate Agreement or Disagreement with the proposed changes

- Agree with all of the changes and accept the proposed balance due

- CAUTION: If you select this option, the IRS will notify the state(s) as well so the taxpayer will most likely receive additional notices from any states that the taxpayer has a filing requirement.

- Taxpayer Signatures - Taxpayer (& spouse if filing Married Filing Joint) must sign and date this section if all changes are acceptable.

- Do not agree with some or all of the changes in the notice

- This option will require responding with supporting documentation to inform the IRS their records are incorrect.

- The IRS will send another notice responding to the taxpayer's dispute and additional actions to be taken.

- Agree with all of the changes and accept the proposed balance due

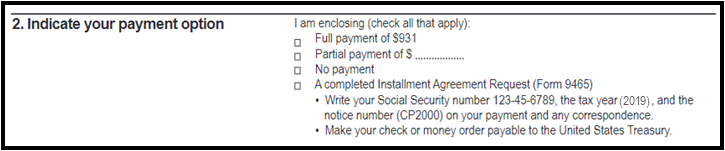

- Indicate Payment Option (if applicable)

- Full payment

- Partial Payment

- No Payment

- Installment Agreement

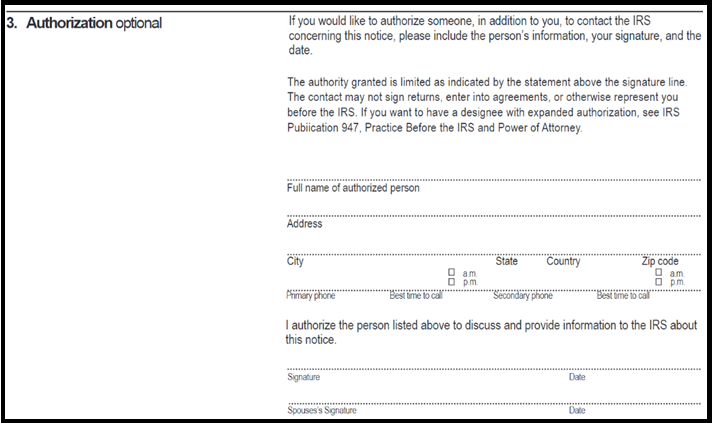

- Authorization (optional)

- A third party can be authorized to speak to the IRS regarding the notice

- Provide name, address, phone number of the authorized party

- Taxpayer Signatures - Taxpayer (& spouse if filing Married Filing Joint) must sign and date this section if authorizing a third party to speak to the IRS regarding the notice.

- NOTE: This authorization gives the third party limited authority when communicating with the IRS. It may be necessary to establish an IRS Power-of-Attorney (POA) to grant additional authority for a third party.

- NOTE: This authorization gives the third party limited authority when communicating with the IRS. It may be necessary to establish an IRS Power-of-Attorney (POA) to grant additional authority for a third party.

- Send the Response Form to the IRS

- If the proposed changes are acceptable, the taxpayer only needs to check the box for "I agree with all changes" and return the Response Form with the appropriate box checked and taxpayer's (and spouse's when applicable) dated signature on the appropriate line(s).

- If the taxpayer disagrees with the proposed changes, the taxpayer will need to check the box "I don't agree with some or all of the changes" and include all documentation necessary to contest the changes with the Response Form.

- Mail the Response Form to the address provided on the notice.

- It is highly recommended that any written communication sent to the IRS be send using a method which offers tracking, such as certified mail or express mail.

- If a fax number is provided on the notice, the taxpayer can also fax the Response Form (and all supporting documentation) to the IRS using the fax number shown on the notice.

Penalties and Interest

Notices may also reflect an assessment of penalties and/or interest added to the calculated amount due. By consulting with a tax professional, there are various strategies that have been used successfully in the past which can be used to request the elimination of an IRS penalty, however, the IRS will ultimately determine if the penalty is abated. Interest is more difficult eliminate and the IRS may reduce/eliminate interest if there has been an unreasonable error on their part.IRS Response

Once a notice response is sent to the IRS, the taxpayer should allow at least 30 days for the IRS to respond.

-

5Not Sure What to do with Your IRS Notice?The CP2000 notice example above is just one of a number of letters the IRS sends out for various reasons. When a notice is received it is important to:

- Pay attention to the response due date,

- Take note of the notice number (i.e., CP2000), and

- Don't panic!

IRS notices are very common and very solvable. If you need help with a notice you have received, reach out to a tax professional who can help you understand your rights as a taxpayer as well as the important of any deadline and consequences of not meeting a deadline. Contact your Project Manager in Soraban as soon as possible and upload a full copy of the notice so we can review it to determine the next steps to get your notice resolved quickly.

Did this answer your question?

If you still have a question, we’re here to help. Contact us