The Anomaly Real Estate Professional Guide for Clients

Our Complete Guide to Real Estate Professional Status (REPS)

Everyone wants to maximize their real estate benefits. Well, let's explore the most powerful way to do this and our experience having generated tens of millions in tax savings from this strategy since 2018.At Anomaly CPA, we’ve worked with dozens of real estate investors to navigate the rules surrounding Real Estate Professional Status (REPS).

For those who qualify, REPS can transform how rental property losses are treated, offering substantial tax benefits.

Our updated 2025 guide provides a step-by-step breakdown of REPS requirements, examples from U.S. Tax Court cases, and tips based on our experience working with the IRS. We have built this guide to dispel the false information that certain online personalities spread and ensure that you are in the most optimal position as an Anomaly member!

-

1What Actually Counts as "Real Estate" for the REPS status?Under IRC Section 469(c)(7)(C), real property trades or businesses include:

- Brokerage

- Development

- Construction

- Management of RE

- Leasing

- Operations & Marketing

Further, if you own 1% of a RE fund, this will NOT count (absent some unique grouping situations). -

2Why Real Estate Professional Status Is a Game-Changer for RE InvestorsUnder the default tax rules, rental property losses are classified as passive losses. IRC 469 is the key to real estate and this states that all real estate income or losses are passive, unless you can prove otherwise.

Passive losses (PALS) mean they can only offset passive income—not wages, self-employment income, or other active income types. For many investors, this limitation results in suspended passive losses that carry forward indefinitely.

Key Point: You will NEVER loss these suspended passive losses, but at Anomaly we believe in the value of Time Value Money, so let's get them to use ASAP.

REPS changes the game. By qualifying as a real estate professional, you can reclassify rental losses as non-passive (some may say "Active", allowing them to offset active/nonpassive income. This creates a powerful opportunity to reduce your taxable income dramatically, particularly when combined with strategies like cost segregation and bonus depreciation.A Practical Example from Our Experience

A married couple with $300,000 in W-2 income purchased a $1.2 million rental property. One spouse qualified as a REP after working with us. After a cost segregation study, 30% of the property qualified for accelerated depreciation (ignoring land allocation for simplicity). With a 60% bonus depreciation rate, they claimed $216,000 in first-year depreciation, creating a nonpassive loss to deduct against one spouses W2 income.

The result? $216k of the $300k of spouse 1 wage's were completely offset, leading to tens of thousands in tax savings! -

3How to Qualify for REPS - The Right WayThe IRS has two key requirements for REPS eligibility...but there is more than meets the eye

1. The Time Test

To qualify, you must:- Spend at least 750 hours per year in real property trades or businesses in which you materially participate, and

- Ensure these activities represent more than 50% of your total working hours for the year in all trades or businesses (including W2 or self employement).

If you work 1,500 hours at a W-2 job, you would need to spend over 1,500 hours on your real estate activities...a scenario that’s nearly impossible unless you scale back your other commitments. Although prospects and clients have argued many times that this is possible...it does come down to the IRS' and US Tax Courts judgement and "believeability" of the facts and circumstances. 9/10 times, they will not believe that a single taxpayer with W2 or married with 2 W2s can acheive this...even if they did.2. Material Participation - what does this even mean?

Beyond meeting the time requirements, you must materially participate in your real estate activities. In typical IRS fashion, they will not 100% define what this means. However, the IRS outlines seven tests for proving material participation. You must hit ONE of the Seven.

The most applicable three tests that you could hit are:- Spending more than 500 hours on a single real estate activity (see grouping info below)

- Being the only participant (or doing the majority of the work). The "significantly all test". If you use property managers or other support on the portfolio, this is likely out. Further, the burden of proof is on YOU to prove their time input.

- Participating for at least 100 hours and more than anyone else. In other words, if your PM spends 101 hours (Tracked) you must spend at least 102 hours.

For the 750-hour test, only one spouse must meet the requirement individually. However, for material participation, both spouses’ hours can be combined to meet the IRS thresholds. As an example, you own a RE Brokerage and spend 2000 hours on this. You are a REP. However, you spend 90 hours on your rentals and your spouse spends 40. This would qualify as materially participating. -

4What Hours Count (and Don’t Count)?When determining whether you meet the REPS requirements, not all activities are treated equally. While there is not a published list, based on our experience and publicly available internal IRS training guides:

Activities That Count Toward REPS & Material Participation:- Advertising, screening, and leasing to tenants

- Collecting rents and managing tenant communications

- Handling repairs, maintenance, and property improvements

- Supervising contractors or managing renovations

- Property inspections and upkeep

- Operational specific travel

- Education and general research (Padilla v. Commissioner, T.C. Summ. Op. 2015-38). No, your Zillow and Podcasting time does not count.

- Investor-level tasks like reviewing financial statements (Barniskis v. Commissioner, T.C. Memo. 1999-258). While accounting related activities COULD count, do not overdo this category.

- Travel time unless it involves specific operational tasks (Truskowsky v. Commissioner, T.C. Summ. Op. 2003-130). Excess travel time will be scrutinized. If you drive or fly for hours, they may limit this.

Example Case: Leyh v. Commissioner - a great use of a log

The taxpayer in this case successfully argued her hours by maintaining detailed logs of property management tasks, such as tenant communications and repairs. However, she avoided claiming travel time, ensuring her logs met IRS standards.

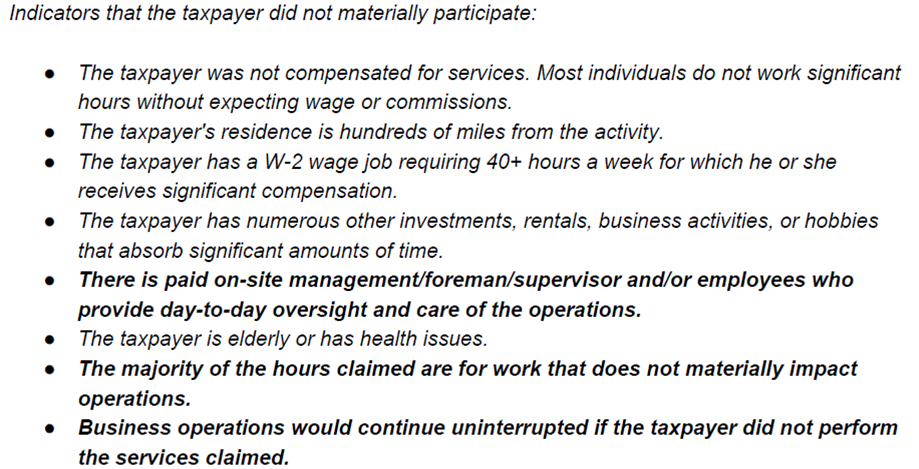

At Anomaly, we have searched high and low for the best info related to REPS and Material Participation...and we found this! The IRS Auditor's training guide:

The last point is key. Would the real estate operations continue uninterrupted if you didn't perform the activity? Let that sink in... -

5How Bonus Depreciation Works with REPSOne of the most powerful tools for REPS status is bonus depreciation, especially when combined with a cost segregation study. Bonus depreciation comes and goes, but as of 2024 it is 60%, scheduled to drop to 40%. However, the Trump admin will likely restore this to 100%!

Key Point: Bonus depreciation percentage is based on the YEAR IN WHICH THE PROPERTY GOES IN SERVICE, NOT THE YEAR OF THE COST SEG!

Example: You buy a property in 2021 in which you are NOT a REP. In 2021, the law was 100% bonus depreciation. Fast forward and in 2024, you are a REP. Anomaly recommends you perform a cost seg. What is your bonus %?- 100% - why? Based on the year in which you placed the asset in service!

A Real Example: Bonus Depreciation in Action

- Property Purchase Price: $1,000,000 (condo, no land value)

- Cost Segregation Identified 30% of Property for Bonus Depreciation (IRC 1245 assets)

- Bonus Depreciation Rate for 2024 Year of Purchase/Service: 60%

When combined with other expenses, the total non-passive loss was $200,000. This was used to offset a client’s $250,000 in active income, reducing their taxable income to $50,000.

Now imagine having several assets and/or doing this every year! You will end up in a very low tax bracket. - 100% - why? Based on the year in which you placed the asset in service!

-

6Is a Cost Segregation Study?Yes. Without this, the IRS will disallow all accelerated deductions. Having read the IRS audit technique guide, we know that the IRS will not like "DIY" efforts by taxpayers. Fortunately, Anomaly offers full service cost segregation studies! Contact your PM for more info to get this started.

-

7Is a Cost Segregation Study Needed in the Year of Purchase or by 12/31?NO! Any cost seg company who markets this to you is lying. In fact, you can perform a cost seg all the way back to 1987 🙂 !

We strategically look for the best opportunity to execute the "CSS". For example:- You buy an asset in 2022 in which your pre-CSS tax rate is 22%. You predict this to be the same for 2023.

- In 2024, your spouse is exercising RSUs and predicts a 35% tax rate

- We would NOT perform the CSS in 2022 and hold until 2024 to take advantage of the higher ROI

-

8The Importance of Detailed Records & The Anomaly Time TrackerAt Anomaly CPA, we’ve seen firsthand how proper documentation can make or break a REPS claim. While the law does not dictate a time log...good luck without one!

The IRS places the burden of proof on the taxpayer, which means your records must be thorough, accurate, and credible.

Best Practices from our experience:- Use the Anomaly Client Time Tracker - make a COPY of this file.

- Keep receipts, correspondence, and photos of completed work to support your logs. Paste them to a new tab

- Ensure your records align with third-party evidence, such as contractor invoices or bank statements.

- Ensure any contractor/property manager give detailed time logs to you, if possible.

In this case, the taxpayer provided detailed time logs supported by invoices and receipts, convincing the Court of their credibility. This reinforced the importance of contemporaneous, specific documentation and led to a better outcome. -

9The Role of Grouping Elections - A misstep waiting to happen!The IRS views each rental property as a separate activity unless you file a grouping election under IRC Section 469. Grouping simplifies the participation test by allowing you to combine hours across all properties.

In other words, you would have to hit the 100 hour/more than anyone else OR 500 hour test on EACH asset, absent the grouping election.

Without Grouping: You must meet material participation tests for each property individually.

With Grouping: All properties are treated as a single activity, making it easier to meet REPS requirements.

Key Point: Anomaly handles this for your! This is a highly technical election and we just want to ensure you understand why we would do this for you.

Example Case Anomaly Examined: Miller v. Commissioner

The taxpayer successfully grouped multiple properties, allowing them to aggregate hours and qualify for REPS. However, without the election, they would have failed the material participation test for several properties.

-

10Challenges and How to Overcome Them

1a. Balancing Real Estate with a Full-Time Job

Full-time employment often disqualifies taxpayers from REPS unless their real estate activities exceed their job hours. There are only 2 known tax court cases, one being a boat pilot, where a FT W2 has beat the IRS in court. Is it worth it to fight this, even if you believe you are a REPS? Likely not.

Our Advice: REPS is more achievable for part-time employees or married couples where one spouse focuses on real estate.1b. But I own an S Corp and I don't do much. Can I qualify?

Ehhh it really depends but it not likely UNLESS you can prove that you have a day to day manager AND your RE time outweighs your S Corp business owner time. How can you prove this? Dual time logs showing your time in both. NOTE - this would still be considered risky as the IRS' default position is likely opposite yours.2. Inflated or Unrealistic Time Logs

Courts routinely reject logs that include vague entries or overstate hours. As an example, if you live in Maine and own assets in Texas...it is NOT reasonable to travel there multiple times per month. You may find it necessary, but trust us, 100% of the time the USTC will throw this time out.

Our Advice: Keep contemporaneous logs with specific details. Do not inflate hours, round hours or use unrealistic travel time.

Logs created after the fact rarely hold up under scrutiny (Pourmirzaie v. Commissioner, T.C. Memo. 2018-26). -

11What about if you are a Real Estate Agent or Broker or RE Developer? Are you automatically in REPS?It comes down to ensuring you materially participate in your assets, beyond generating REPS from your brokerage work:

More than half your total working hours across all jobs and businesses must be spent on real estate activities.

This is where owning a brokerage can help, as your primary occupation is already centered on real estate.

Example:

A taxpayer works 1,200 hours annually managing their brokerage business (that they 100% own) and 300 hours managing their rental properties.

They also spend 500 hours on non-real estate activities, such as investments or consulting.- Total Real Estate Hours: 1,500 (brokerage + rentals)

- Total Working Hours: 2,000

- Result: The taxpayer spends more than half their working hours (1,500 ÷ 2,000 = 75%) on real estate, meeting this test.

- The 300 hours are > anyone else, the grouping election has been made, therefore, they pass material participation.

-

12The Most Common Questions we Receive on REPS:

Can travel time count toward REPS?

The IRS typically does not consider travel time as qualifying hours unless it directly involves operational tasks, such as inspecting properties or managing contractors on-site. Traveling to "check on it" will be scrutinized. That being said, at Anomaly, we look at each situation in depth. You WILL receive credit for some travel time, but it should not be the majority of your time.Do education or research hours count?

Generally, no. Time spent on education or research, such as attending seminars or researching potential investments, does not count toward REPS unless it directly impacts the ongoing operations of your current rental properties. Some taxpayers have sucessfully argued this, while others have not.What are Other Strategies or Benefits of REPS?

1) No NIIT! If you are a REP, both your ongoing rental income and any sale of an asset is NOT subject to the dreaed 3.8% net investment income tax

2) The Lazy 1031 Exchange - check out are KB on that!

3) Increased Business Expenses - we may recommend you create a Management Company for your active management which will allow you to deduct a home office, all business supplies, business autos etc.

4) Spousal Qualificiation - this is likely the most common situation we see. One spouse works or owns a business and the other works part time or does not work. By strategizing and working towards REPS for the nonworking spouse, you can generate a MASSIVE ROI. However, this spouse must actually perform the work to get to REPS, which may be difficult if they have no prior experience. We recommend this is a phased approach over several years.

5) ROTH Conversions at 0% - we have executed this several times. Check out our ROTH Conversion Guide.

6) Ok, I have read this guide and there is no change I am a REP. Am I out of luck?

Not necessarily! The STR Loophole can be a great strategy OR you can buy a building in which your business operates.

Contact us for more info on both.

If both are these are not options, then we would recommend a PIGS strategy! Invest in a long term passive income generator such as mineral rights or ATMs. Check out our Member Webinars on these.

Did this answer your question?

If you still have a question, we’re here to help. Contact us