S Corp Payroll Guide

A lot of business owners directly or indirectly operate through an S Corporation. There is a LOT of bad information out there surrounding the payroll requirements in an S Corp, which we will look to clarify and add strategic elements to in this guide.

-

1Key Terms:Reasonable Compensation - the IRS required payroll that an S Corp owner must pay. This is based on the facts and circumstances. Payroll means you must have a W2 wage by 12/31.

199A - the QBI or Qualified Small Business Income Tax Deductions for all "pass through" business owners.

-

2Basics of S Corporation Compensation and the "Why"

- S Corporation Distributions vs. Salary: Owners can receive both a salary and distributions from the corporation's profits.

- The salary is subject to employment taxes (Social Security and Medicare), while distributions are not.

- Remember, whether or not you "distribute" the cash, you are still taxed on it!

- Don't fall for the trap "If I don't take money out, I won't pay taxes". No! You pay taxes on your profit, not your distributions.

- Reasonable Compensation is not "optional"! The IRS Requires Reasonable Compensation to be paid to the officer(s) of the S Corp based on their duties. We could list a hundred tax court cases on this issue and the trends are the same. If you pay $0 in RC, you will 100% lose under audit UNLESS you take $0 from the company.

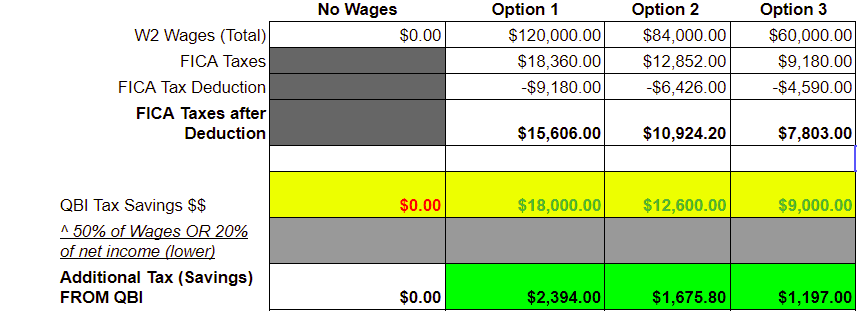

- Target Ratio: At Anomaly, we first want to look at the facts and circumstances and the owner's input into the business. If justifiable, we want to target a 27.775% ratio between the Profit and the Owner's wage.

- For example, if your annual profit is $100,000, we'd want an owner's compensation/target of $28,000.

- This is the most advantageous ratio which will INCREASE your QBI deduction and keep payroll taxes as low as possible.

- This is the most advantageous ratio which will INCREASE your QBI deduction and keep payroll taxes as low as possible.

- For example, if your annual profit is $100,000, we'd want an owner's compensation/target of $28,000.

Steps to Set Up:

Sign up your NEW S Corp for Gusto here. NOTE - you may need to use a different email if you have a separate Gusto account for another business.- State Tax Set Up - for all state instructions to ensure your payroll account is registered, check out these step by step guides.

- Note - all states are different. The guides will get you most of the way there but if you have questions, please reach out. We only support GUSTO payroll.

- Link your Business Bank Account

- Link your Personal Bank Account

- S Corporation Distributions vs. Salary: Owners can receive both a salary and distributions from the corporation's profits.

-

3Strategic Elements: Maximizing QBI DeductionThe Tax Cuts and Jobs Act introduced the QBI deduction, allowing eligible taxpayers to deduct up to 20% of their qualified business income.

This is where we see new business owners go wrong! The QBI deduction partially looks at the W2 wages paid in a business, including the owner's wage.

IF YOU HAVE NO OTHER EMPLOYEE'S DO NOT SKIP THIS SECTION!!!- Balancing Act: A lower salary might temporarily increase the QBI deduction since the deduction is based on net business income, if you are BELOW the thresholds ($170k and $340k single/MFJ). However, the salary must still be "reasonable" to avoid IRS penalties.

- Timing of Payroll - it does not matter much. You can generally run payroll at any time BEFORE year end but it is best practice to run it at least quarterly in order to avoid pesky letters and notices from the IRS or various state agencies.

- If you are ABOVE $170/$340k of total income:

- Wage Limitations: For higher income taxpayers, the QBI deduction can be limited based on W-2 wages paid by the business.

- Therefore, increasing wages might increase the available QBI deduction.

- High Income Taxpayers - we will recommend you INCREASE your wage to INCREASE your QBI deduction! This can be an excellent strategy when you family income is over the phase out thresholds in a given year.

- If you are above these numbers and pay a $0 wage, your QBI deduction is now $0!

- Retirement Planning Implications- if you have a Solo or Regular 401k or SEP IRA and you pay $0 in wages...you will receive a whopping $0 of retirement benefits if you do not pay a reasonable comp!

- Be sure to work with us to plan out much much you'd like to contribute by YE.

-

4Using the W2 Withholding Loophole as an S Corp Owner to Lower your Estimated Taxes

Did this answer your question?

If you still have a question, we’re here to help. Contact us